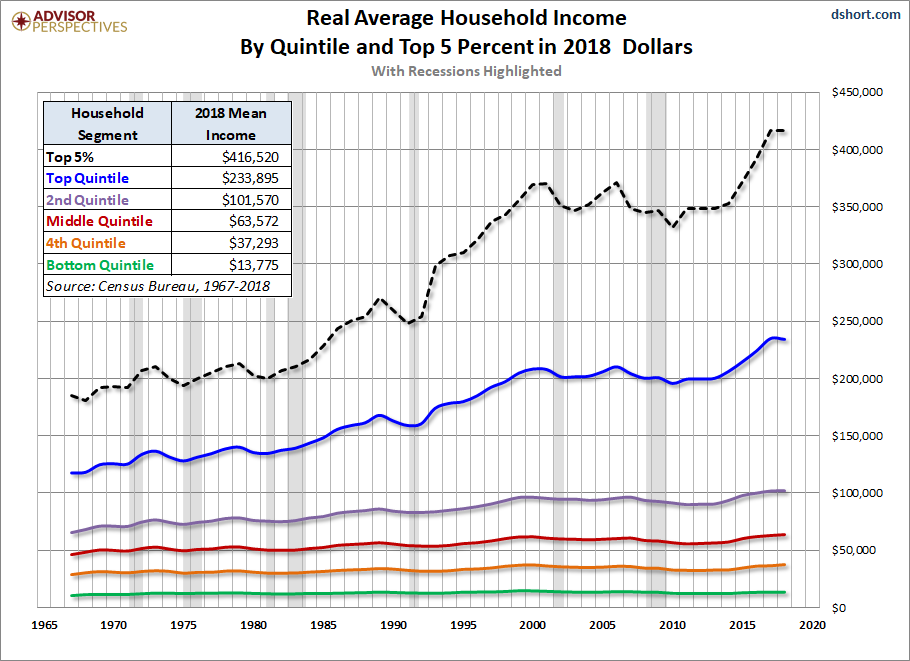

A prior post made an effort to gain greater analytical clarity concerning the unfairness involved in the separation between the “one percent” economy and the rest of us. In what ways is the wealth owned by the super-billionaires an “unfair” extraction from the rest of US society? How can we account for the very rapid accumulation of wealth in the hands of the richest 1 percent of US wealth holders since 1980? The answer seems to largely turn on the rapid expansion in wealth represented by the US stock market over that period, and the fact that a very small number of wealth holders captured the lion’s share of these gains. The following graph shows a five-fold increase in the value of the US equity market in part of that time, from about $12 trillion in 1998 to $52 trillion in 2024. The wealth owned by the top 1% of households increased at about the same rate, which implies that this class rode the wave to wealth right along with the stock market in those years. “Corporate equities and mutual fund shares” are the largest component by far of the wealth portfolios of the top .1% and 1%, as reflected in the second chart below, produced by the Federal Reserve.

It was shown in the earlier post that the growth of the super-billionaires’ share of the nation’s wealth cannot be explained in normal “business profit” terms. (For reference, the top twenty billionaires in the US own 2.8 trillion dollars of wealth; link.) Rather, the bulk of the wealth now held by individuals like Mark Zuckerberg, Elon Musk, and Jeff Bezos represents the rapid appreciation of value in capital markets of the companies in which they have large ownership stakes. The companies themselves do not generate billions of dollars in dividends; rather, their total stock value has witnessed billions of dollars in gains over very short periods of time.

So why should we think this is in any way unfair? How is it exploitative? Is it not more like the fortunate visitor to “Antiques Road Show” who finds that the forgotten painting in the closet is in fact an early Picasso and is worth millions on the art market? This is good fortune for the owners of the canvas, but surely these facts don’t suggest “exploitation” of anyone else. Perhaps not in the case of the Antiques Road Show guest; but the majority owner of Amazon, Tesla, or Meta is in a different set of circumstances. Rather, the existence and continuing success of these companies depends on background conditions to which all sectors and components of the US economy contribute: a stable system of law and regulation, a robust education and research sector, a skilled workforce, an infrastructure of roads, ports, rail lines, fiber optic cables, and electricity providers. The value of US companies is at least in part a system effect: it is facilitated and constituted by a vast network of private and public stakeholders, all of whom contribute ultimately to the success of the company and the value it finds within the equity market. So the value of the US company is inseparable from the large and heterogeneous economic and political system in which it operates, and the increase in value over time of the US company reflects the continuing contribution expected by the investing public from the functioning of that system.

It will be said, of course, that the companies and their executives themselves contribute to the value that investors attribute to them: innovative products, good management systems, efficient decision-making, appropriate personnel practices, “entrepreneurship” and risk-taking. This is true. But it is also true that these contributions represent only a portion of the increase in value that the company experiences over time. The system effects described here represent an independent and important component of that substantial increase in value. So we might say that “system-created increase in value” is the uncompensated part of wealth creation in today’s economy. Companies pay little or nothing to cover the cost of these system-level inputs on which they depend; these are the inverse of “externalities”, in that they are benefits taken without compensation from the public (rather than harms imposed without compensation on the public). And these system-created increments in value constitute a very important part of the increase in value that they experience over time.

We might therefore look at “system-created increase in value” as the counterpart to “unpaid labor time” in the classic theory of exploitation. It is the source of wealth (profit) that the owners of wealth derive simply in virtue of their position in the property system and in their opportunity to benefit from the economic system upon which they depend. But now it does not derive from the “surplus value” contributed to profits by each worker, but rather from the synergies created by the socio-economic system as a whole.

It should also be noted that the ability of private companies to “extract” value from system-level inputs without compensation depends on their ability collectively to influence government policy. Therefore owners of private companies and stock wealth have strong incentives to shape the decision-making of elected officials, government policy makers, the fiscal system, and the regulatory process. This reinforces the arguments made by Thomas Volscho and Nathan Kelly in “The Rise of the Super-Rich: Power Resources, Taxes, Financial Markets, and the Dynamics of the Top 1 Percent, 1949 to 2008” (link). It follows, then, that achieving powerful influence on public policy and economic rule-making is not just a hobby for the oligarchy; it is an existential necessity.

This analysis of “system-input exploitation” has important consequences for distributive justice. If the whole of society contributes to the creation of the system-level properties that generate a significant fraction of the new wealth created in the past forty years, then surely fairness requires that all participants should receive some part of the gains. It would seem logical for the non-wealth-holding stakeholders — workers, farmers, and uncompensated contributors to social reproduction — to demand economic reforms that direct a fair share of that new wealth to the benefit of the whole population.

The previous post suggested one possible mechanism that would do this. The post discusses a hypothetical “public investment fund” that “would be automatically vested with ownership shares of businesses and corporations as they are created and grow, and that would function as a ‘wealth reserve’ for all citizens”. This would constitute a large and growing asset to be used for the benefit of the whole of society. In that discussion a distribution of gains resulting in public ownership of 1/3 of all capital was considered. Such a division would reduce (though not eliminate) the most extreme inequalities of wealth that currently exist, and would provide a financial basis for a more genuine “free community of equals” through the secure establishment of a high level of the resources most needed — healthcare, education and training, environmental protection, and provisioning of basic human needs for children, the disabled, the elderly, and the unemployed.

This idea of a public investment fund corresponding to the “systemic value creation” of the economy might go a long way towards the securing political values embodied in John Rawls’s concept of a “property-owning democracy” (link). Rawls argues that “the equal worth of liberty” is incompatible with a society in which political influence is proportional to wealth and where wealth is extremely unequally distributed. Wealth inequality of this magnitude means that the oligarch’s liberty and worth are magnified many times relative to the ordinary citizen’s situation. The creation of a substantial public investment fund representing the value created by our social, economic, and political system of cooperation would reduce the total proportion of the total value of the economy that the multi-billionaire class is able to expropriate. It would create real property entitlements for the great majority of society, and it would redress the current horrendous inequality of political influence that exists between the super-rich and the ordinary citizen.